Quantitative Strategic Asset Allocation, easy for you.

Riskfolio-Lib is a library for making quantitative strategic asset allocation or portfolio optimization in Python made in Peru 🇵🇪. It is built on top of cvxpy and closely integrated with pandas data structures.

Some of key functionalities that Riskfolio-Lib offers:

- Portfolio optimization with 4 objective functions (Minimum Risk, Maximum Return, Maximum Risk Adjusted Return Ratio and Maximum Utility Function)

- Portfolio optimization with 10 convex risk measures (Std. Dev., MAD, CVaR, Maximum Drawdown, among others)

- Risk Parity Portfolio optimization with 7 convex risk measures (Std. Dev., MAD, CVaR, Maximum Drawdown, among others)

- Worst Case Mean Variance Portfolio optimization.

- Portfolio optimization with Black Litterman model.

- Portfolio optimization with Risk Factors model.

- Portfolio optimization with constraints on tracking error and turnover.

- Portfolio optimization with short positions and leveraged portfolios.

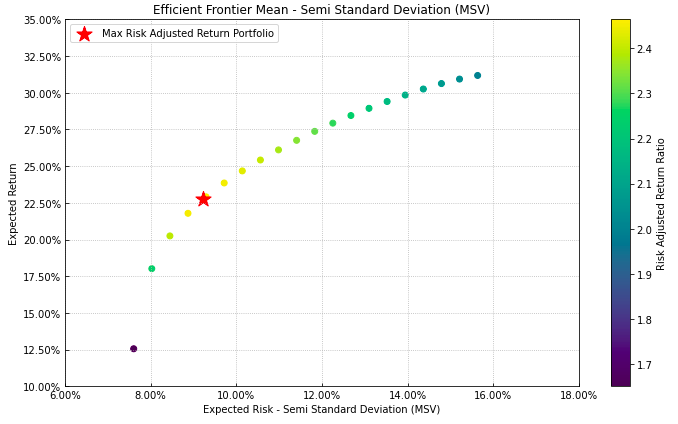

- Tools for build efficient frontier for 10 risk measures.

- Tools for build linear constraints on assets, asset classes and risk factors.

- Tools for build views on assets and asset classes.

- Tools for calculate risk measures.

- Tools for calculate risk contributions per asset.

- Tools for calculate uncertainty sets for mean vector and covariance matrix.

- Tools for estimate loadings matrix (Stepwise Regression and Principal Components Regression).

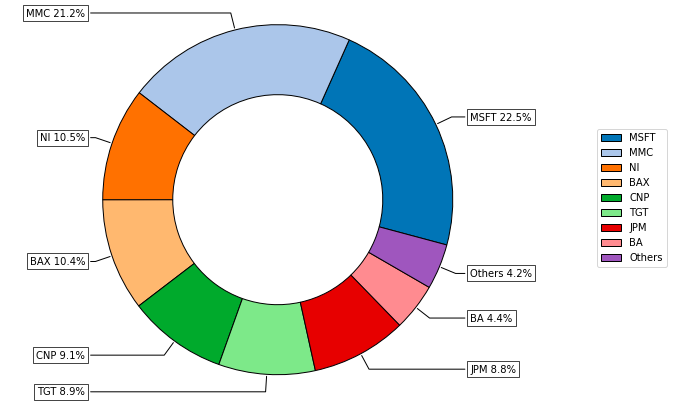

- Tools for visualizing portfolio properties and risk measures.

Online documentation is available at Documentation.

The docs include a tutorial with examples that shows the capacities of Riskfolio-Lib.

Riskfolio-Lib supports Python 3.7+.

Installation requires:

- numpy >= 1.17.0

- scipy >= 1.1.0

- pandas >= 1.0.0

- matplotlib >= 3.3.0

- cvxpy >= 1.0.15

- scikit-learn >= 0.22.0

- statsmodels >= 0.10.1

- arch >= 4.15

The latest stable release (and older versions) can be installed from PyPI:

pip install riskfolio-lib

Riskfolio-Lib development takes place on Github: https://github.com/dcajasn/Riskfolio-Lib

The plan for this module is to add more functions that will be very useful to asset managers.

- Mean Entropic Risk Optimization Portfolios.

- Add functions to estimate Duration, Convexity, Key Rate Durations and Convexities of bonds without embedded options (for loadings matrix).

- Add more functions based on suggestion of users.