A python package for time series forecasting with scikit-learn estimators.

tspiral is not a library that works as a wrapper for other tools and methods for time series forecasting. tspiral directly provides scikit-learn estimators for time series forecasting. It leverages the benefit of using scikit-learn syntax and components to easily access the open source ecosystem built on top of the scikit-learn community. It easily maps a complex time series forecasting problems into a tabular supervised regression task, solving it with a standard approach.

tspiral provides 4 optimized forecasting techniques:

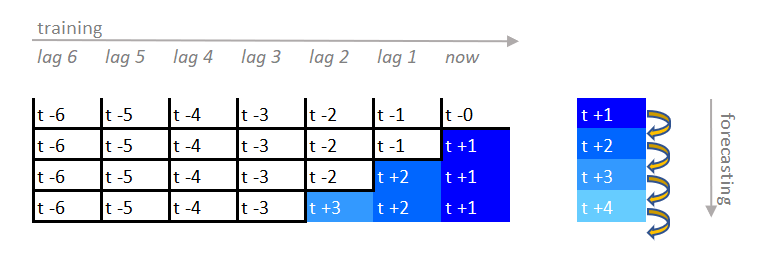

- Recursive Forecasting

Lagged target features are combined with exogenous regressors (if provided) and lagged exogenous features (if specified). A scikit-learn compatible regressor is fitted on the whole merged data. The fitted estimator is called iteratively to predict multiple steps ahead.

Which in a compact way we can summarize in:

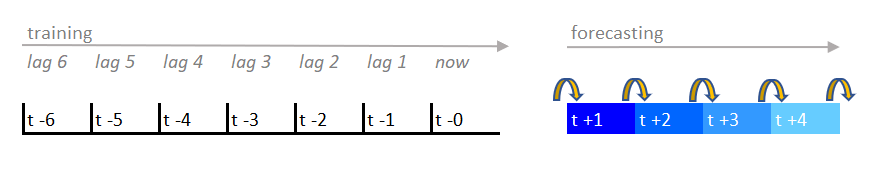

- Direct Forecasting

A scikit-learn compatible regressor is fitted on the lagged data for each time step to forecast.

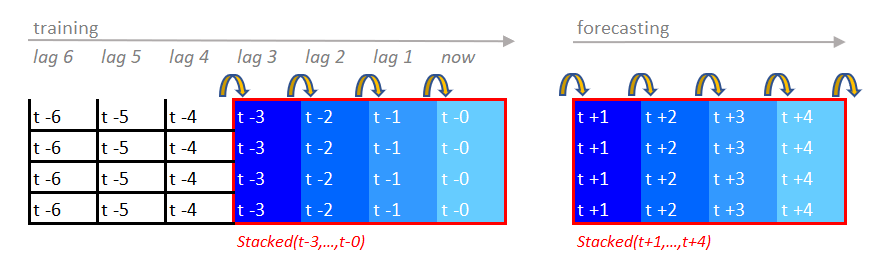

- Stacking Forecasting

Multiple recursive time series forecasters are fitted and combined on the final portion of the training data with a meta-learner.

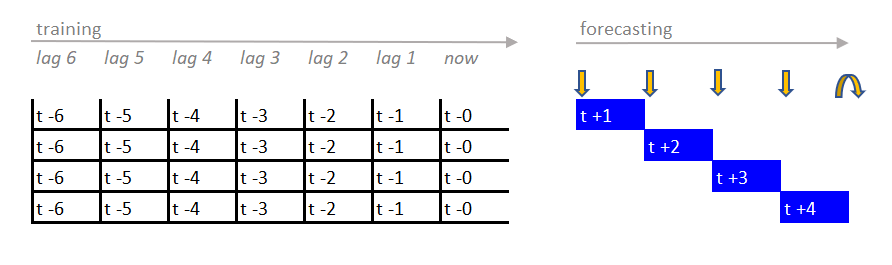

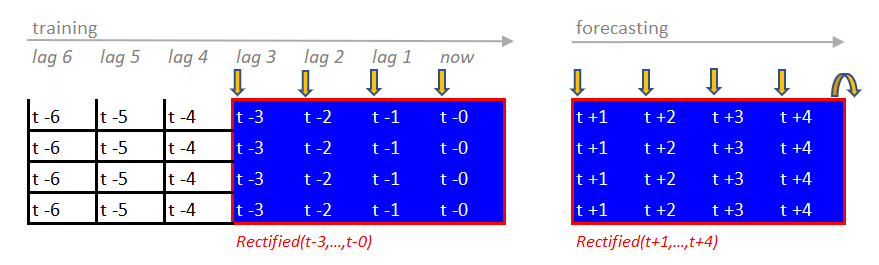

- Rectified Forecasting

Multiple recursive time series forecasters are fitted on different sliding window training bunches. Forecasts are adjusted and combined fitting a meta-learner for each forecasting step.

Multivariate time series forecasting is natively supported for all the forecasting methods available.

pip install --upgrade tspiralThe module depends only on NumPy and Scikit-Learn (>=0.24.2). Python 3.6 or above is supported.

- How to Improve Recursive Time Series Forecasting

- Time Series Forecasting with Feature Selection: Why you may need it

- Forecast Time Series with Missing Values: Beyond Linear Interpolation

- Time Series Forecasting with Conformal Prediction Intervals: Scikit-Learn is All you Need

- Recursive Forecasting

import numpy as np

from sklearn.linear_model import Ridge

from tsprial.forecasting import ForecastingCascade

timesteps = 400

e = np.random.normal(0,1, (timesteps,))

y = 2*np.sin(np.arange(timesteps)*(2*np.pi/24))+e

model = ForecastingCascade(

Ridge(),

lags=range(1,24+1),

use_exog=False,

accept_nan=False

)

model.fit(None, y)

forecasts = model.predict(np.arange(24*3))- Direct Forecasting

import numpy as np

from sklearn.linear_model import Ridge

from tsprial.forecasting import ForecastingChain

timesteps = 400

e = np.random.normal(0,1, (timesteps,))

y = 2*np.sin(np.arange(timesteps)*(2*np.pi/24))+e

model = ForecastingChain(

Ridge(),

n_estimators=24,

lags=range(1,24+1),

use_exog=False,

accept_nan=False

)

model.fit(None, y)

forecasts = model.predict(np.arange(24*3))- Stacking Forecasting

import numpy as np

from sklearn.linear_model import Ridge

from sklearn.tree import DecisionTreeRegressor

from tsprial.forecasting import ForecastingStacked

timesteps = 400

e = np.random.normal(0,1, (timesteps,))

y = 2*np.sin(np.arange(timesteps)*(2*np.pi/24))+e

model = ForecastingStacked(

[Ridge(), DecisionTreeRegressor()],

test_size=24*3,

lags=range(1,24+1),

use_exog=False

)

model.fit(None, y)

forecasts = model.predict(np.arange(24*3))- Rectified Forecasting

import numpy as np

from sklearn.linear_model import Ridge

from tsprial.forecasting import ForecastingRectified

timesteps = 400

e = np.random.normal(0,1, (timesteps,))

y = 2*np.sin(np.arange(timesteps)*(2*np.pi/24))+e

model = ForecastingRectified(

Ridge(),

n_estimators=200,

test_size=24*3,

lags=range(1,24+1),

use_exog=False

)

model.fit(None, y)

forecasts = model.predict(np.arange(24*3))More examples in the notebooks folder.